How Fintechs and Neobanks Should Think About Adding DeFi Yield

The custody question has a clean answer. The product decisions are harder.

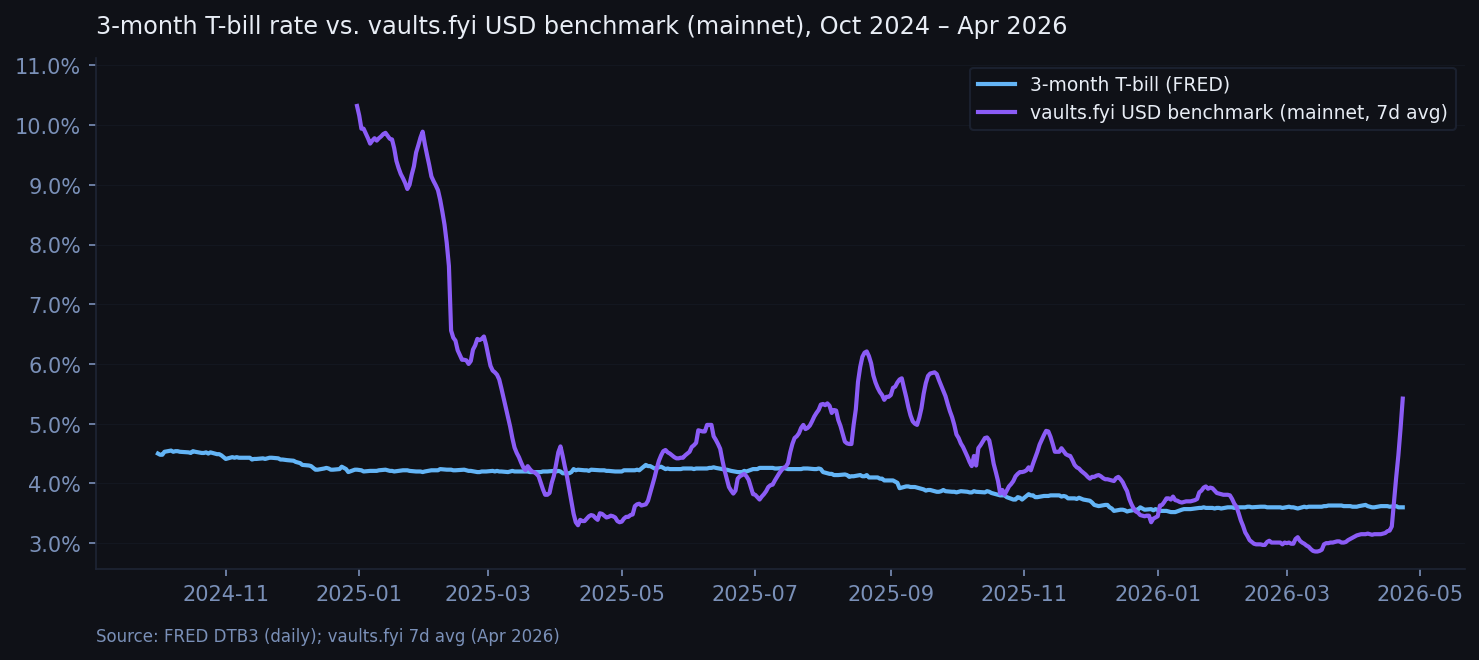

4.5% to 2.8%. That compression in neobank cash yields happened over 18 months, and every product review now includes the same question from leadership: can we offer crypto yield without taking on custody risk?

The answer is yes, with the right infrastructure. The path is narrower than most people assume, and the most important decision is not technical. It is a compliance question that happens to have a technical answer.

Why fintechs are looking at DeFi yield now

Three pressures converged this year:

- Traditional yields on cash and short-term instruments came down. A neobank that competed on 4.5% APY in 2024 is now offering closer to 2.8% and watching retention erode.

- Crypto-native savings products maintained healthy yields. Stablecoin yield across major DeFi protocols held a 3-6% range on blue-chip assets through 2025 and into 2026. Users noticed.

- U.S. and EU regulatory clarity gave fintechs a framework to reason about stablecoins and on-chain products. Most compliance teams no longer start the conversation from "no." They start it from "show me the custody model."

The product question shifted from "should we offer any crypto yield at all" to "which architecture lets us offer it without inheriting custody risk."

What custody actually looks like in DeFi

The word "custody" does a lot of work here. It is worth pinning down.

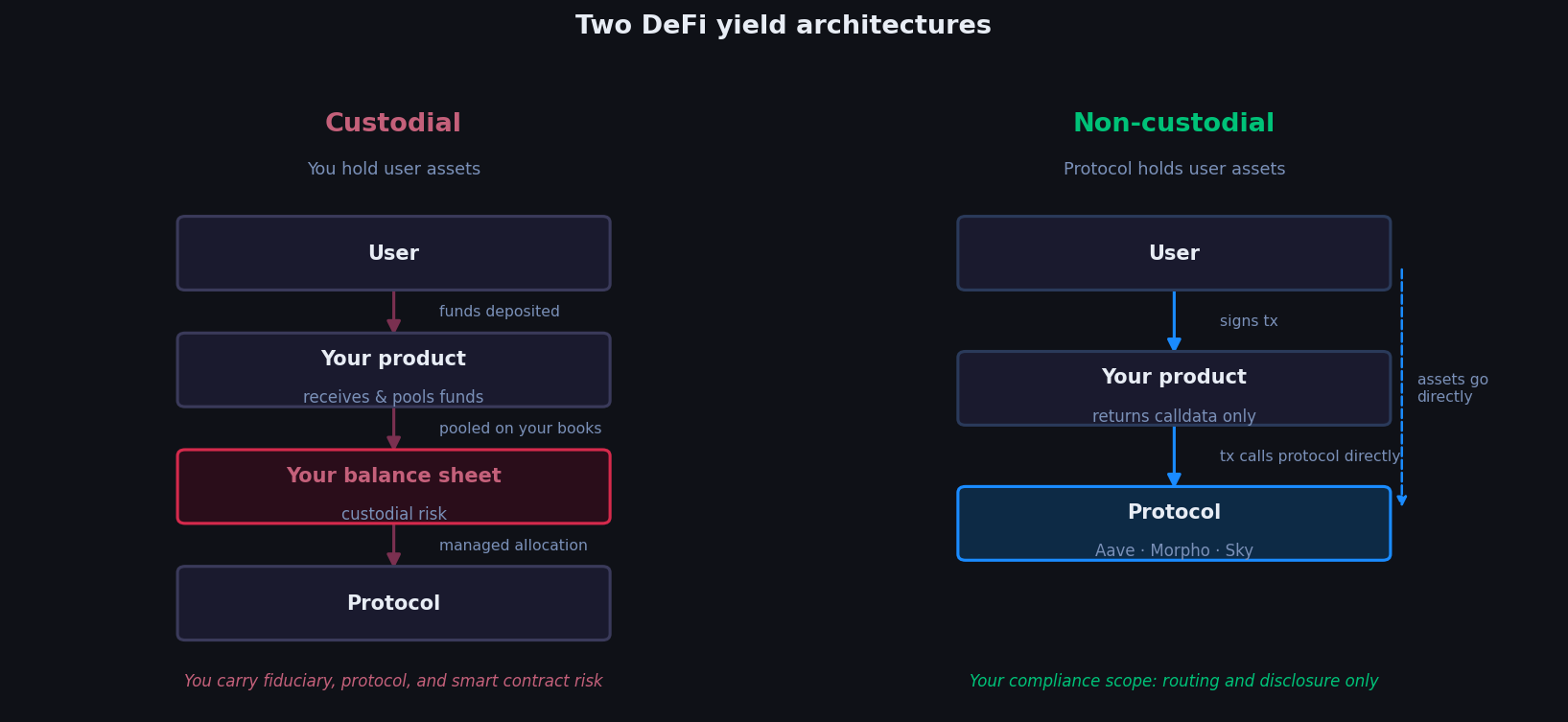

A custodial yield product takes user funds onto your balance sheet, pools them, and pays out yield from a managed allocation. You become a fiduciary. You take protocol risk, smart contract risk, and operational risk. This is how the failed centralized yield products of the last cycle worked, and why their collapse was existential for the companies running them.

A non-custodial yield product never takes user funds. The user signs a transaction that moves their own assets directly into the underlying protocol. The protocol holds the assets. You hold nothing. Your compliance scope is routing and disclosure, not asset custody.

For a fintech, non-custodial is the only architecture that reliably survives a compliance review. Custodial DeFi yield requires you to become a regulated entity on a new axis. Non-custodial lets you add a product surface without changing your regulatory footprint.

The vaults.fyi Earn API is built around this distinction. When a user deposits through your product, the transaction calls the protocol directly. No vaults.fyi contract in the middle, no pooled deposit, no wrapper token to account for. User assets go from your wallet infrastructure into Aave, Morpho, Sky, or whichever protocol you allowlist. We return the calldata. The user signs it.

Where yield fits in a neobank product surface

Start from the product surface, not the infrastructure.

- Inside the existing savings or earn tab. The user already expects a yield number. You add a stablecoin yield option alongside the cash savings line. Same mental model, different underlying asset. Lowest friction, broadest reach.

- As a new asset class in the investing tab. Treat stablecoin yield as an investment product with disclosures, suitability checks, and a separate risk profile. Higher friction, cleaner compliance framing.

- As a dedicated crypto tab. Users self-select into a different risk profile. You can offer a wider vault set with more detailed disclosure because the audience is pre-qualified.

Your compliance counsel will likely push you toward one of these before you finish the conversation. The savings tab needs the tightest disclosure language and a narrow allowlist. The crypto tab can run looser. Pick the surface before you pick the vaults.

The compliance conversation

Three things will come up when you bring this to legal and compliance.

- Custody. Non-custodial architecture resolves it. Show your counsel the transaction flow. The user's wallet calls the protocol. Your product never holds the asset.

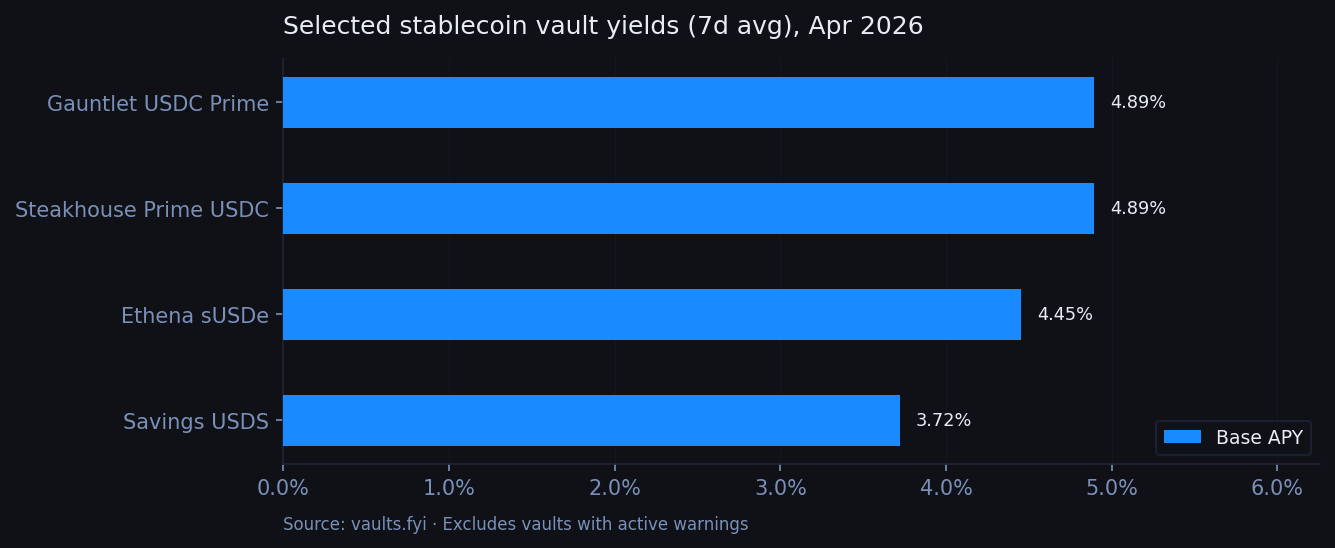

- Asset selection. Not every vault is appropriate for a regulated retail audience. Most fintechs ship with a conservative allowlist: stablecoin vaults only, blue-chip protocols (Aave, Morpho, Sky), trusted curators (Gauntlet, Steakhouse, Sentora), minimum TVL floors, and a risk score threshold. vaults.fyi exposes these as query parameters so your allowlist lives in a single config, not a series of separate integrations.

- Disclosure. Users need to understand that yield is variable, smart contract risk is real, and funds move on-chain. Every vault in the API response carries a

warningsarray you can surface directly in your UI.

Build vs. buy, quickly

Most fintech engineering teams underestimate this scope. Per-chain contract differences alone add weeks, and that is before you build the risk filtering layer. Building in-house means integrating each protocol separately, writing deposit and redemption logic for each, and maintaining it as protocols evolve.

An API integration means one codebase, one config file of allowlist rules, and new protocols that appear automatically. The full allowlist for a conservative fintech deployment looks something like this:

allowedProtocols=aave,morpho,sky&minTvl=10000000&minVaultScore=80Build makes sense if you only care about a single protocol, need deep custom UX inside the vault interaction, or are building infrastructure you intend to sell. For a fintech whose product surface is checking, savings, and a simple earn tab, buying is usually the right call.

Proof point

Kraken's Beholder helps users create an account and route deposits into Tydro, Aave, Fluid, Sky, and more onchain products across multiple networks.

The earn flow is fully non-custodial, powered by a single vaults.fyi API integration that connects Beholder to multiple allowlisted protocols. It is a different regulatory footprint from a typical neobank, with the same architectural conclusion.

For the full technical walkthrough, covering vault data, transaction building, and portfolio endpoints, see the wallet and app integration guide.

What to do next

If you are scoping this, there are three potential steps to take:

- Get legal and compliance in a room and ask what would let them say yes. Most of the time the answer is "show me a non-custodial flow and a conservative allowlist." If that is the answer, you know what you are building.

- Pick the product surface. Savings tab, investing tab, or crypto tab. Do not pick all three on day one.

- Scope against real infrastructure.

Our full docs are available at docs.vaults.fyi.

To walk through how this maps to your product, reach out to ryan@wallfacer.io.